All Categories

Featured

Table of Contents

Note, nonetheless, that this doesn't state anything regarding adjusting for rising cost of living. On the plus side, also if you presume your choice would certainly be to purchase the stock exchange for those seven years, which you 'd get a 10 percent annual return (which is far from specific, specifically in the coming decade), this $8208 a year would be greater than 4 percent of the resulting small supply worth.

Example of a single-premium deferred annuity (with a 25-year deferment), with four settlement choices. The regular monthly payment here is highest for the "joint-life-only" option, at $1258 (164 percent greater than with the instant annuity).

The means you acquire the annuity will figure out the solution to that question. If you buy an annuity with pre-tax dollars, your premium reduces your taxed income for that year. According to , purchasing an annuity inside a Roth plan results in tax-free payments.

How do I get started with an Immediate Annuities?

The consultant's initial step was to create a detailed financial plan for you, and afterwards discuss (a) how the recommended annuity suits your overall strategy, (b) what alternatives s/he taken into consideration, and (c) exactly how such options would or would not have actually caused lower or greater compensation for the advisor, and (d) why the annuity is the exceptional option for you. - Immediate annuities

Of program, a consultant might attempt pressing annuities also if they're not the very best fit for your situation and goals. The reason could be as benign as it is the only item they market, so they fall prey to the typical, "If all you have in your toolbox is a hammer, pretty soon everything starts resembling a nail." While the consultant in this scenario might not be underhanded, it increases the risk that an annuity is a poor option for you.

Secure Annuities

Because annuities typically pay the representative selling them a lot greater compensations than what s/he would obtain for spending your cash in shared funds - Tax-deferred annuities, not to mention the no compensations s/he would certainly obtain if you purchase no-load common funds, there is a large motivation for representatives to press annuities, and the a lot more challenging the far better ()

A dishonest advisor suggests rolling that quantity into new "much better" funds that just occur to lug a 4 percent sales tons. Accept this, and the expert pockets $20,000 of your $500,000, and the funds aren't most likely to carry out much better (unless you picked much more badly to start with). In the exact same example, the consultant might guide you to buy a challenging annuity with that $500,000, one that pays him or her an 8 percent payment.

The expert tries to hurry your decision, asserting the offer will quickly vanish. It might without a doubt, but there will likely be similar offers later on. The advisor hasn't determined just how annuity payments will certainly be taxed. The consultant hasn't disclosed his/her payment and/or the costs you'll be charged and/or hasn't revealed you the influence of those on your ultimate settlements, and/or the settlement and/or costs are unacceptably high.

Present rate of interest prices, and hence forecasted payments, are historically reduced. Also if an annuity is right for you, do your due diligence in comparing annuities offered by brokers vs. no-load ones marketed by the providing business.

What should I know before buying an Guaranteed Return Annuities?

The stream of month-to-month payments from Social Safety is comparable to those of a delayed annuity. A 2017 comparative evaluation made a comprehensive contrast. The following are a few of the most significant factors. Considering that annuities are volunteer, individuals buying them typically self-select as having a longer-than-average life span.

Social Safety and security advantages are totally indexed to the CPI, while annuities either have no rising cost of living defense or at many offer a set percentage yearly boost that may or might not compensate for inflation completely. This kind of rider, just like anything else that raises the insurance provider's risk, requires you to pay even more for the annuity, or approve reduced payments.

What happens if I outlive my Retirement Annuities?

Disclaimer: This write-up is meant for informative objectives only, and must not be considered economic advice. You need to consult a financial professional before making any type of significant financial decisions. My career has had numerous uncertain weave. A MSc in theoretical physics, PhD in experimental high-energy physics, postdoc in particle detector R&D, research study placement in speculative cosmic-ray physics (consisting of a number of sees to Antarctica), a quick stint at a little design services business sustaining NASA, adhered to by beginning my own tiny consulting method sustaining NASA jobs and programs.

Because annuities are planned for retirement, tax obligations and charges may use. Principal Defense of Fixed Annuities. Never lose principal as a result of market efficiency as repaired annuities are not spent in the marketplace. Even during market declines, your cash will certainly not be influenced and you will certainly not shed cash. Diverse Financial Investment Options.

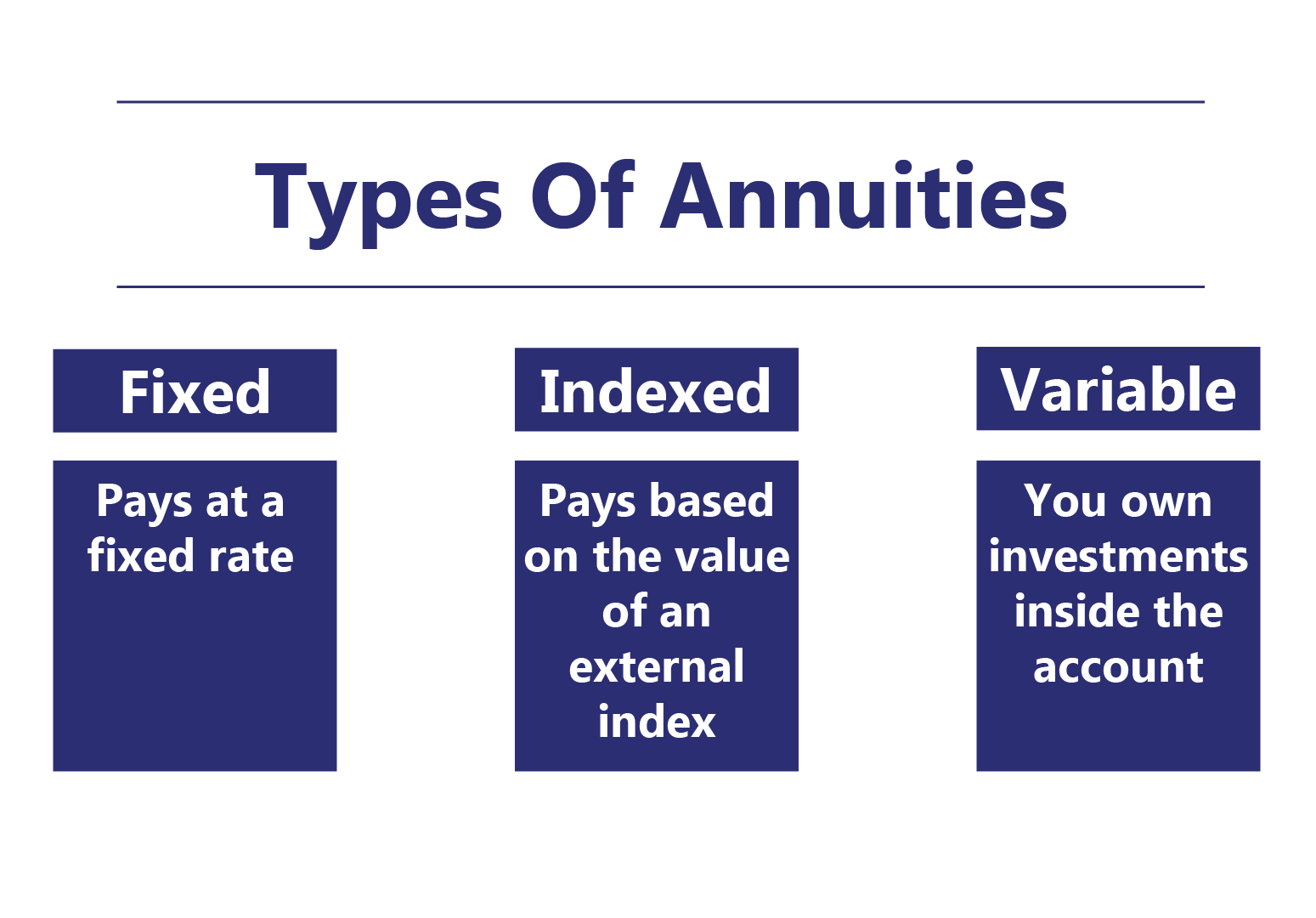

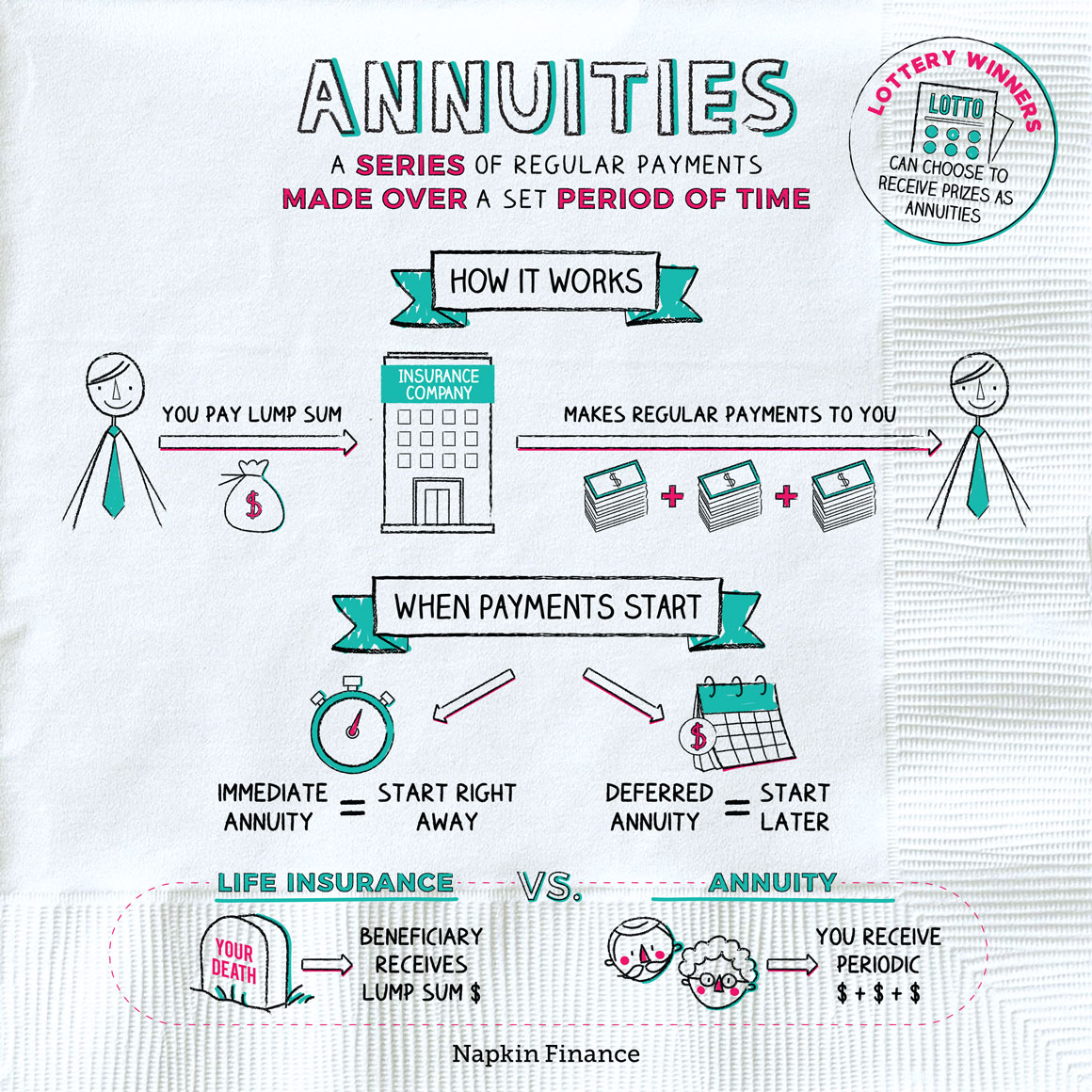

Immediate annuities. Utilized by those who desire reliable revenue quickly (or within one year of acquisition). With it, you can customize earnings to fit your requirements and produce revenue that lasts permanently. Deferred annuities: For those that intend to grow their money over time, but are willing to delay access to the cash till retired life years.

How can an Long-term Care Annuities help me with estate planning?

Variable annuities: Supplies greater possibility for growth by investing your cash in investment alternatives you pick and the capacity to rebalance your profile based upon your preferences and in a manner that lines up with transforming monetary goals. With taken care of annuities, the company spends the funds and offers a passion price to the customer.

When a death insurance claim accompanies an annuity, it is necessary to have a called beneficiary in the contract. Different choices exist for annuity fatality advantages, depending on the agreement and insurance provider. Picking a reimbursement or "period certain" option in your annuity supplies a survivor benefit if you die early.

What does an Retirement Income From Annuities include?

Naming a beneficiary various other than the estate can aid this procedure go extra efficiently, and can help make sure that the proceeds go to whoever the individual desired the cash to go to instead of experiencing probate. When existing, a death advantage is immediately consisted of with your contract. Depending on the kind of annuity you purchase, you may be able to add boosted survivor benefit and attributes, but there can be additional costs or costs connected with these add-ons.

{kind=link}

Table of Contents

Latest Posts

Decoding Fixed Index Annuity Vs Variable Annuity A Comprehensive Guide to Investment Choices Breaking Down the Basics of Investment Plans Benefits of Immediate Fixed Annuity Vs Variable Annuity Why Ch

Breaking Down Your Investment Choices A Comprehensive Guide to Investment Choices Defining Retirement Income Fixed Vs Variable Annuity Advantages and Disadvantages of Variable Annuities Vs Fixed Annui

Highlighting the Key Features of Long-Term Investments Everything You Need to Know About Financial Strategies Defining the Right Financial Strategy Advantages and Disadvantages of Different Retirement

More

Latest Posts